Looming Debt Restructuring

As one of the largest corporate debt restructuring exercises in recent years is about to begin, it begs the question of whether some local companies have taken on too much debt prior to the pandemic.

The case of Sapura Energy Bhd , saddled with unpaid debts and payables to the tune of RM15bil, has been widely reported.

, saddled with unpaid debts and payables to the tune of RM15bil, has been widely reported.

While Sapura Energy has a laid out plan on how it intends to go about fixing this problem, discussions with its nervous lenders and creditors is a different matter.

Sapura Energy may seek the assistance of the country’s Credit Debt Restructuring Committee (CDRC), like how some, albeit smaller oil and gas listed outfits in Malaysia, dealt with their crumbling debt that they found difficult to service, especially after the 2014 oil crash.

CDRC first reared its head following the 1997 Asian Financial Crisis when many large Malaysian companies were hit by a devalued ringgit, putting them in the impossible situation of having to service their debt, much of which was denominated in United States dollars.

Fast forward to today, and you have a situation where cheap debt has been available since 2009.

CDRC was set up by the government to provide companies and their creditors a platform to work out feasible, speedier and less cumbersome debt resolutions without having to resort to legal proceedings.

The CDRC was first set up following the 1997/1998 financial crisis and ceased operations in 2002, only to be revived in 2009 as a means to help financially ailing companies.

Fast forward to today and the question is, are some Malaysian listed companies overgeared?

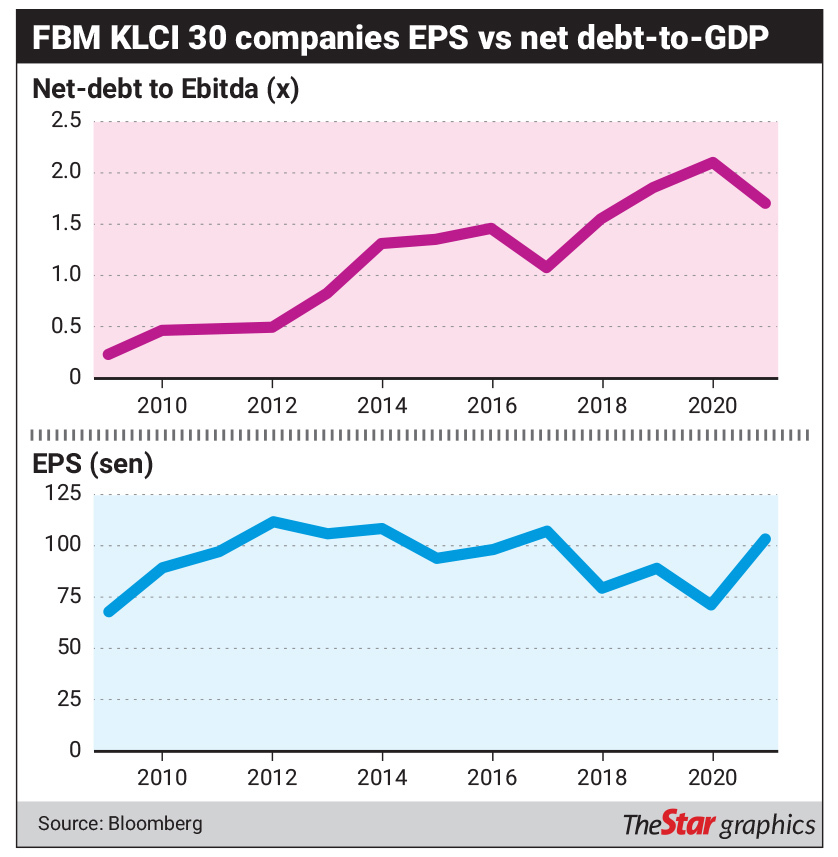

One interesting data point is this – the debt-to-earnings before interest, taxes, depreciation, and amortisation (Ebitda) ratio of top Malaysian public listed companies has octupled since 2009, going by data from Bloomberg (see chart).

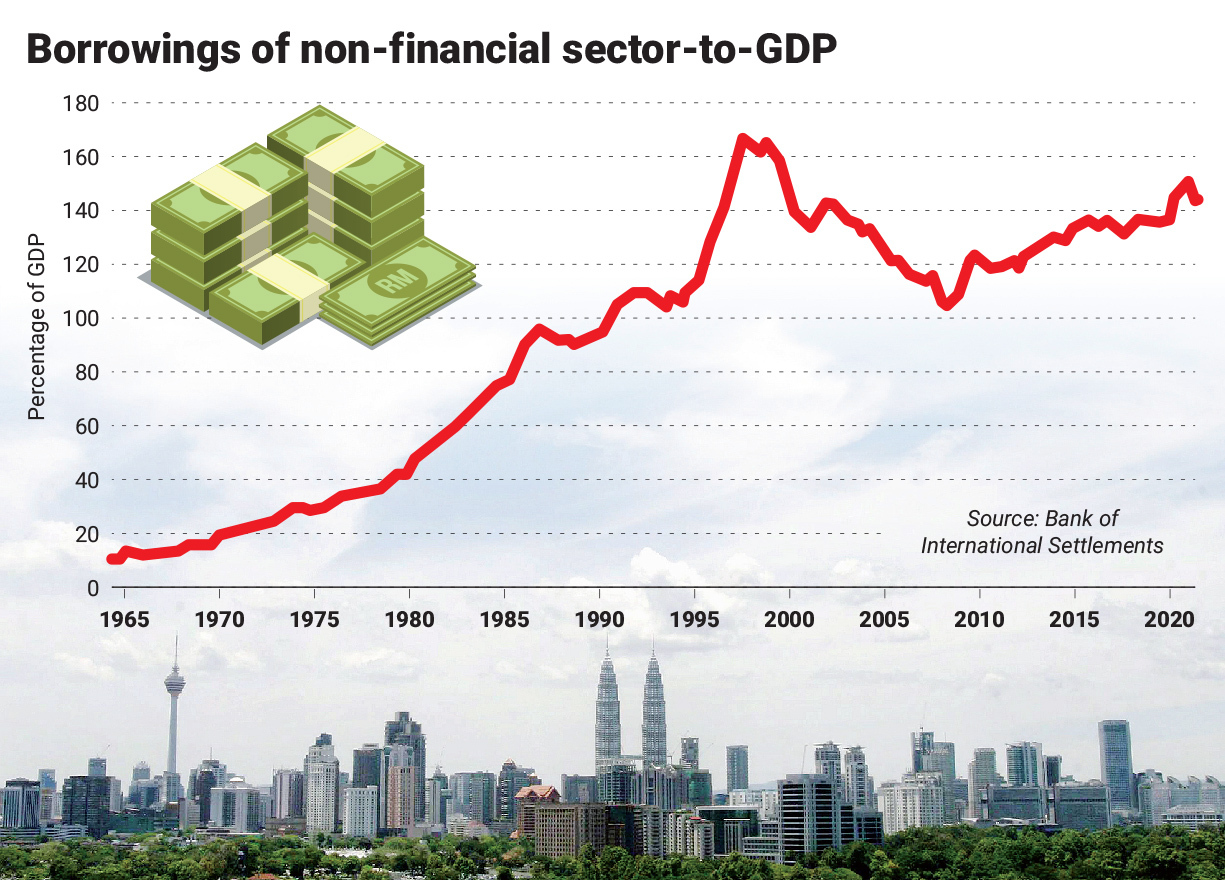

Another is this: the debt levels of Malaysian corporations (excluding financial institutions) has grown by more than 30% since 2009.

According to the Bank of International Settlements, the debt level of Malaysia’s non-financial corporate sector had grown to 150% of the country’s gross domestic product (GDP) in 2021.

This is higher than regional countries such as Indonesia, whose corporate debt stands at 42.4% to GDP, while India’s is at 87.7%.

The global debt rate stands at 98%, notes the International Monetary Fund. Making matters worse is the fact that earnings of Malaysian listed companies have also been on a downtrend since 2012.

Earnings per share (EPS) of FBM KLCI companies stood at 111.8 sen in 2012, dropping to 71.13 sen in 2020 and stood at 104.72 sen at the end of last year.

Supporting this, is the statement recently made by Bursa Malaysia chairman Tan Sri Abdul Wahid Omar during the launch of the PLC Transformation Programme.

In a report, Wahid said listed companies have posted a decline in profitability between 2016 and 2019, where the earnings of the FBM KLCI component stocks fell by 4.3% while the earnings for the FBM Emas component stocks, the much broader index with many more stocks, dropped by 1.2% over the four-year period.

This was the period before the Covid-19 pandemic hit the global economy.

And based on the MSCI Country Index between 2020 and 2022, the market’s forecast earnings per share and compound annual growth rate were among the lowest in the region at 2.5% compared with Indonesia and Thailand, which were at 22.5% and 10.3% respectively.

The Ratings Agency of Malaysia (RAM) also revealed some interesting numbers.

In an analysis of the performance of 725 non-financial listed companies in Malaysia, RAM noted that after a promising export-driven recovery in the first half of 2021, growth retreated to minus 4.5% in the third quarter of 2021.

“The reimposition of the nationwide MCO from June to its gradual easing in mid-July dampened the economy and concurrently saw third quarter 2021 corporate earnings take a beating,” the report said.

But what about their debt servicing abilities? On this issue, the RAM report opined that all seems well for now.

“Over half (55.2%) of the 725 companies in our sample recorded lower Ebitda year-on-year, while one in five recorded operating losses. Despite the weaker earnings, leverage metrics as measured by both Ebitda to debt and debt to equity ratios reveal still-robust balance sheets and debt servicing aptitude.

“Companies’ liquidity positions have also remained adequate to cushion against rising uncertainties.

“Bursa firms have sufficient reserves to sustain four months of operating expenses, with most of these reserves being in liquid cash and cash equivalents.”

A cry for help

Several companies have already sought help with their debt, especially those that loaded on more debt prior to the onslaught of the Covid-19 pandemic.

For example, at least four other listed companies had recently gone to the CDRC to sort out their debt issues last year.

These include property and hospitality company Sentoria Group Bhd, and oil and gas service firms Nam Cheong, Daya Materials Bhd and Alam Maritim Resources Bhd.

Those are smaller firms though. This year, it looks like larger firms are seeking debt restructurings.

Recently, AirAsia X Bhd went through a whooping RM33bil debt restructuring, which saw its creditors write off 99.5% of their investment.

In other words, the airlines will pay just 0.5% of the debt owed.

Omni Capital Partners founding partner Scott Lim expects more urgent debt restructuring on the horizon if companies cannot recover fast enough from the Covid-19 pandemic, and to generate enough cash flow to cover their debts.

“It is normal for companies to borrow to grow their businesses.

“But, in Malaysia we have many companies that are in the ‘traditional sectors’ that require high capital expenditure such as property development, O&G, plantations and utilities.

“The earnings growth of these ‘traditional industries’ has been tepid over the past six to seven years as they are also competing with new sectors such as technology,” he tells StarBizWeek.

He points out that the local stock market main index, the FBM KLCI, has not been growing over the last seven to 10 years due to the unexciting corporate earnings.

“The Malaysian stock market is one of the worst performing markets in the region since 2009.

“There are structural issues that need to be addressed such as whether companies’ digitalisation adoption is moving fast enough.

Areca Capital Sdn Bhd CEO Danny Wong advised companies that need to restructure their debt to do it as soon as possible, especially with central banks around the world increasing their interest rates.

“Whenever there is a crisis, debt levels will increase or spike because companies’ revenue will be disrupted, unless these companies have sizable cash reserves.

“We do expect more companies to go through restructuring to help restore their balance sheet, which is crucial to continue their business and facilitate further growth,” he says.

Last week, the Federal Reserve (Fed) announced its first interest-rate hike of 25 basis points to 0.5%, and signalled there would be more hikes this year.

Back in Malaysia, economists expect Bank Negara to take a more conservative stance.

Expectations are for at least one rate hike of 25 basis points this year.

When corporations take borrowings to grow their business, earnings growth should be bigger than the debt, but that has not been the case in some listed companies for the past five to seven years.

According to data by Bloomberg, the 30 companies that make up the components of the FBM KLCI had experienced a flattish earnings per share (EPS) growth from 2010 to 2017.

EPS for these companies have been on a decline since then.

Whereas, the net-debt per share of these companies have been growing at a 24% compounded annual growth rate from 2009-2019, the Bloomberg data shows.

As an example, Tenaga Nasional Bhd’s total debt has more than tripled to RM80.9bil in 2021 from RM22.62bil in 2009.

Wong reckons that even before the Covid-19 pandemic, there had already been a trend of some companies borrowing money to support their cash flows.

“Our corporate EPS has been on a decline since 2014, after the Fed’s tapering quantitative easing measures because many companies did not change their business model and are raising debt to support their existing business.

“In addition, our Industrial 4.0 adoptions are not moving fast enough.

“We have to reduce our dependence on foreign labour and adopt new sectors to support growth moving forward,” he says.

An oily issue

The sector that is the most affected by debt problems is oil and gas (O&G). Ever since the 2014 oil crash, many players in the sector had been badly hit, especially those that had taken on much debt.

Bursa-listed oil and gas service equipment companies such as Daya Materials Bhd, Barakah Offshore Bhd, Perisai Petroleum Teknologi Bhd, Velesto Energy Bhd (previously known UMW Oil And Gas Corp Bhd), Icon Offshore Bhd, Alam Maritim Resources Bhd and TH Heavy Engineering Bhd, all had overgeared during the boom days of high oil prices, which was just prior to the September 2014 oil price crash.

Some of these companies had earlier ended up with the CDRC.

One example is Perisai Petroleum, which was a darling stock on Bursa Malaysia prior to the 2014 O&G crash. The company had to be liquidated after its regularisation plan did not pan out.

Now, all eyes are on how Sapura Energy is going to get out of its debt doldrums. It is worth noting that the company had gone through various corporate exercises since 2014. These ranged from asset disposals, capital injections and debt refinancing. It also had undertaken massive asset impairments on its books.

The exercise that caught the market’s attention was the massive RM4bil cash call in 2019 that saw the emergence of Permodalan Nasional Bhd becoming Sapura Energy’s single largest shareholder with a 40% stake.

However, despite that massive capital injection, Sapura Energy continued to be in the red. In fact it had to take on a RM10.3bil debt refinancing last year. Last week it posted its largest quarterly loss of RM6.61bil for its fourth quarter ended Jan 31, 2022. Its full year net loss was RM8.9bil. It had made a RM3.3bil provision for impairment on goodwill, mainly on its drilling assets.

While Sapura Energy has for some time had a massive order book running into billions of ringgit, analysts point out that the group struggles due to its high operational costs and losses from legacy contracts and low margins projects.

“Sapura Energy blamed its state of affairs on ‘legacy contracts’ that did not factor in Covid-19- related compliance costs, but that is not likely to be the only issue, in our view.

“The company’s misfortunes are probably due to over-optimistic cost estimates, aggressive bid prices in past efforts to win contracts and possible management competency issues,” CGS-CIMB Research said in a recent report.

Two weeks ago, Sapura Energy proposed a restructuring of its RM15bil of debt that would involve banks, vendors and contractors. The company has been facing several winding-up petitions by some of its vendors over unpaid monies.

However, Sapura Energy managed to secure a restraining order – effective for three months from March 10 – to restrain and suspend legal proceedings against it, while enabling the group and its subsidiaries to engage with its creditors without being disrupted by the threat of litigation. It was also given a court order to summon meetings with its creditors to consider a proposed scheme of arrangement as part of its debt restructuring plan.

Sapura Energy’s proposed debt restructuring plan has also been filed with the stock exchange. The 44-page document entails that for every RM1 debt owned, 25 sen will be refinanced, 20 sen will be converted into perpetual non-tradeable notes that have a 5% coupon per annum. This perpetual paper is convertible into ordinary shares of Sapura Energy from its fourth year.

The remaining 55 sen will be converted to perpetual non-tradable zero-coupon notes issued by Sapura Energy. These notes will be converted into shares in Sapura Energy’s subsidiaries, namely Sapura Drilling Sdn Bhd, Sapura Technology Solutions Sdn Bhd and Sapura Geosciences Sdn Bhd, in the fourth year.

It is left to be seen if creditors will accept the proposal, considering it involves a significant haircut. Furthermore, a debt restructuring expert reckons that in order for companies like Sapura Energy to sustain their cash flows and operations, a white knight is likely needed to come in with fresh capital.

One of the lenders involved is the country’s largest bank by assets, Malayan Banking Bhd, a 49%-unit of PNB.

A banking analyst expects that the RM10bil debt of Sapura Energy is unlikely to have a significant impact on the banking sector.

“It is not a single bank exposure and the banks may have already provided for this over the years. The impact will not be significant to the banking sector,” the analyst says, adding that, “It should be noted that Sapura Enegy’s debts are backed by assets.”

Sapura Energy’s assets include its remaining 50% stake in exploration and production arm SapuraOMV.

In 2018, the company sold 50% of SapuraOMV to Austria’s OMV Aktiengesellschaft for US$890mil (RM3.7bil).

Sapura Energy also has other sizeable assets including its fabrication yard in Lumut, six semi-tender drilling rigs and six tender assist rigs, as well as some vessels.

Sapura Energy started an asset monetisation plan last year and is in talks with potential buyers.

The problems with stressed cash flows and the inability to service debt is certainly not limited to the oil and gas sector.

Industry observers reckon that more such restructurings will be taking place now even with small and medium sized companies, as debt reprieves come to an end.

https://www.thestar.com.my/business/business-news/2022/03/26/looming-debt-restructuring