Annual Statement Report 2023

Dear Family, Friends and Partners,

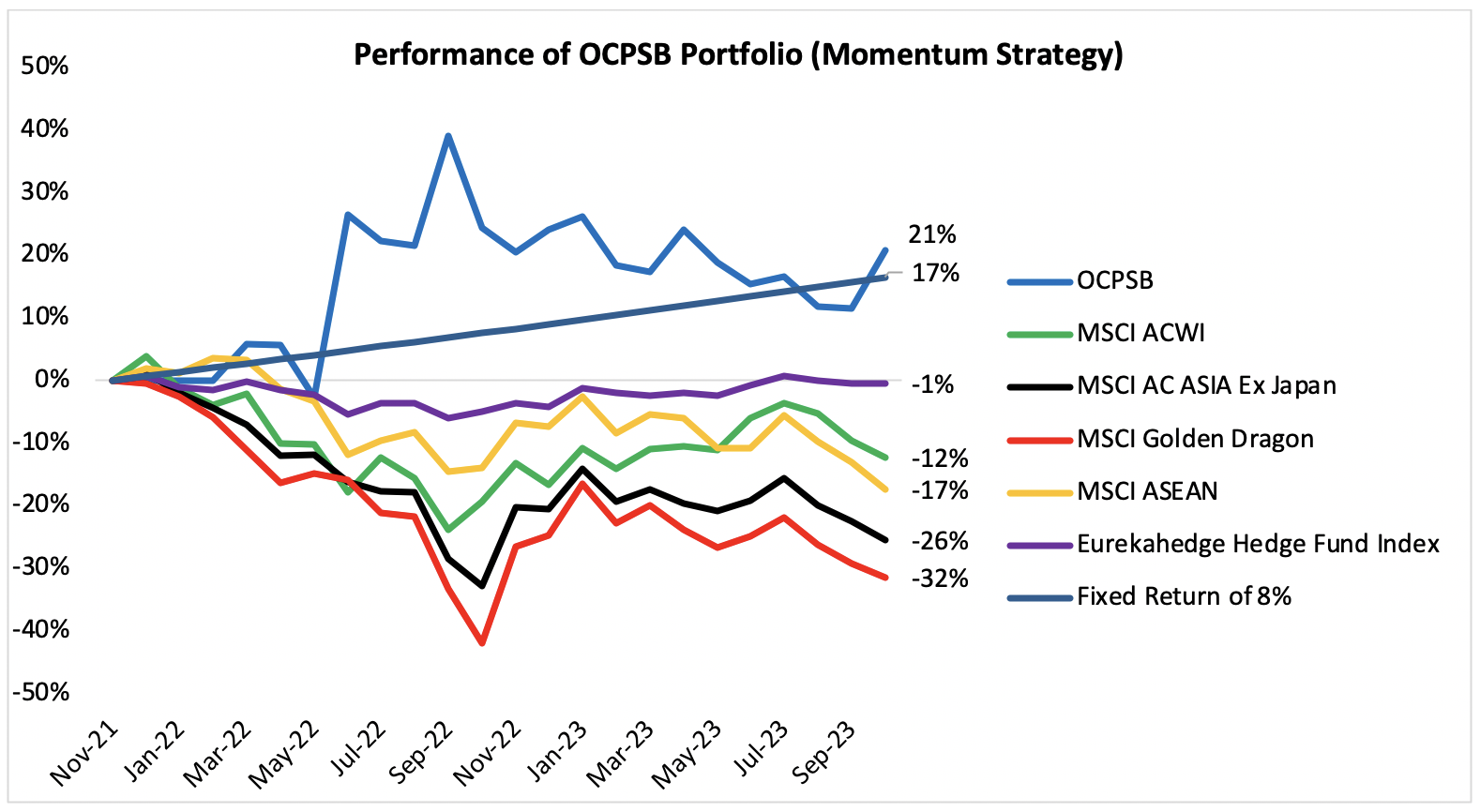

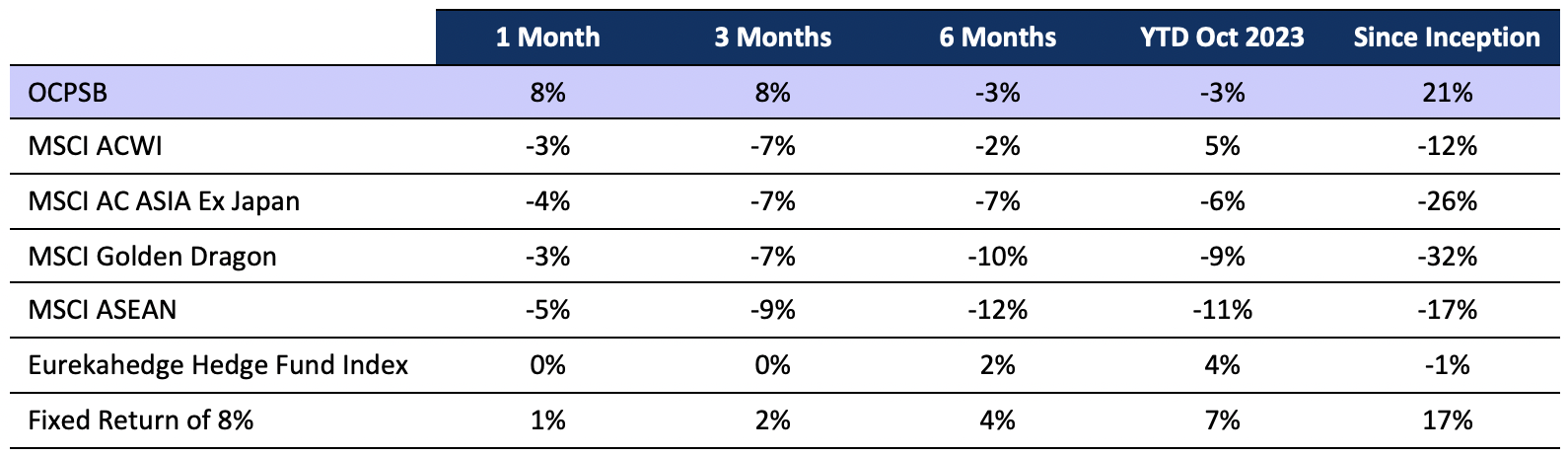

Summary of the company’s investment performance in 2023:

In 2023, the markets experienced a challenging year, primarily influenced by:

• Uncertainties on global economic slowdown and recession;

• The unprecedented tightening of global monetary policy;

• Supply disruptions on the global bond markets;

• Middle East war, with fear of stagflation; and

• Increasing geopolitical risks.

OCPSB portfolio registered -3% year-to-date and Time Weighted Rate of Return (TWRR) of 21% since inception on November 2021. The underperformance this year can be attributed to the persistent weakening of emerging markets (with attractive valuations), notably in China and the ASEAN region. Nevertheless, we have outperformed all other benchmarks as stated in the table above. Currently, the portfolio remains fully invested and market uncertainties will remain high. Looking ahead, we intend to maintain our focus on investing more in emerging markets. This decision is based on the alluring valuations they present, which, in our assessment, offer a more favourable risk-reward ratio when compared to many developed markets.

Market & Economic Outlook

THe performance of asset classes in 2023 has been noteworthy, with Bitcoin emerging as the top performer, outshining traditional assets like stocks and bonds. Despite trading in a consolidation phase, Bitcoin has delivered exceptional gains, reflecting its growing status as a legitimate investment option. The robust performance of developed markets in 2023 can be largely attributed to the prevailing AI sentiment. This reflects the growing importance and positive sentiment surrounding AI-driven technologies and investments, which have significantly contributed to the success of these markets. However, it’s worth noting that the sustainability of this performance may be in question in the short-term.

Rising interest rates are posing challenges for governments, particularly in low-income and frontier countries, as they struggle to secure hard currency borrowing with foreign investors demanding higher returns, resulting in increased coupon rates for bond issuances. However, these sovereign debt concerns aren’t limited to less developed nations, as even advanced economies have seen a surge in longer-term interest rates. In contrast, major emerging economies, benefiting from stronger economic fundamentals, are better positioned to weather the storm, though they have not escaped the impact of rising rates, with foreign portfolio investment flows slowing. Notably, China has experienced a significant outflow of foreign investment due in part to concerns about its property sector, impacting investor confidence. The property downturn in China is not solely a result of structural factors; it is also driven by intended government policies. In the years between 2000 and 2012, the Chinese government actively encouraged debt-fuelled investments, a substantial portion of which flowed into unproductive real estate sectors. This led to excessive leverage, unsustainable property prices, and an overcapacity issue. As a response to the financial risks posed by this situation and a desire to boost the contribution of private consumption to the economy, Beijing had little choice but to guide investment back to more sustainable levels, thereby addressing these concerns prior to a robust rebound in the Chinese market.

The ongoing tightening of credit and the persistence of high Treasury yields are driven by a delicate interplay between supply and demand factors. As the government issues more Treasury bonds, supply pressure increases. However, the strength of demand may not be sufficient to counteract the upward pressure on yields. Expectations of rising interest rates, inflation concerns, and evolving investor preferences contribute to this dynamic.

Major economies like the United States, Europe, China, and the ASEAN region are currently in different phases of their economic cycles. The U.S. is in a late-cycle expansion with rising recession risks, Europe has entered a recession, ASEAN is in a consolidation phase awaiting fresh growth momentum, and China is grappling with a late-cycle contraction despite policy stimulus. Meanwhile, the Middle East remains a potential hotspot for the escalation of conflicts. Recent developments, including the announcement of war plans and targets for the Gaza Strip, indicate ongoing tensions in the region. Geopolitical risks, combined with other factors, have the potential to impact global financial markets.

In conclusion, the evolving economic landscape calls for a flexible and refined approach to investment. Investors should seize new opportunities by focusing on active investment strategies designed to achieve returns that surpass benchmark expectations. The dispersion of valuations among different markets and asset classes creates room for diversification and risk mitigation, especially in a world marked by economic uncertainties and shifting dynamics.

Best Regards,

Scott Lim

Founding Partner

30th November 2023